Cobalt Consumer Index (11.14.22)

The following contains our view on the market and the interesting dynamics that inform our investing in consumer technology businesses

Some quotes from public company executives below, over the last few weeks discussing consumer spend across various sectors.

Travel demand is on fire

"We exceeded expectations, and Q3 was also the first quarter that we surpassed 2019 levels on a consolidated revenue basis at 107%, accelerating from 99% last quarter. We have a lot of confidence in the consumer. We haven't seen anything change. No signs of trading down. We -- I think we referenced Europe as being different from the U.S. But beyond that, the consumer has been strong." - Tripadvisor CEO

"The strength we have experienced over the past several quarters has continued into the fourth quarter. Our EBITDA during October was an all-time monthly record for the property. Similarly, our forward-looking indicators also remain quite strong despite well-known macro concerns as room bookings are pacing at or above pre-COVID levels on substantially higher ADRs." - Wynn Resorts CEO

Should expect to see promotions

“...given the slowdown in consumer demand and the inventory buildup in the marketplace, the level of discounting that we have been experiencing since September was more significant than initially expected. Increased promotional activity, given the high inventory in the marketplace, will continue to weigh on our gross margin during the remainder of the year" - Adidas CFO

Consumers could be in trouble

"...the external environment continues to be challenging, particularly for those less affluent borrowers with limited access to credit at the core of Upstart's mission. Consumers have simultaneously whittled personal savings rates from pre-pandemic levels of roughly 9% down to 3.3% in Q3, a level not seen since the great financial crisis, and have swapped credit card balances to record highs. Savings rates have dwindled, and credit card balances have inflated to pay for a continuing expansion in real consumption, so far with no corresponding increase in either real wages or labor force participation since the advent of COVID. As a consequence, defaults are on the rise. Industry-wide data shows that less affluent borrowers are leading the way with impairment levels on unsecured personal loans that are about twice as high as before the onset of COVID. By comparison, highly affluent borrowers are now roughly back to being in line with pre-COVID impairment levels, although they continue to rise" - Upstart CFO

Consumers will be affected by layoffs

Big tech companies have been conducting large layoffs going into Q4

Companies pulling back on ad spend into the holidays

"It's hard to say exactly what's going to happen in Q4, but we are seeing signs that Q4 is going to be worse in terms of the ad market than Q3 was, I mean we're seeing lots of big categories, pull back telecom, insurance. We're even seeing telemarketers planning on reducing their spending in Q4. I think traditionally, Q4 is a very – the holiday season is typically the strongest period for a lot of companies, including Roku. But companies are pulling back their ad budgets because they're uncertain if there will be a recession or not. And so a lot of Q4 ad campaigns are being cancelled" - Roku CEO

Top 10 Companies by EV / NTM Revenue Multiple

Auto Trader continues to be the only consumer company trading above 10x on NTM multiple. Mean and Median are relatively flat from the last report

Summary of All Multiples

Mean and Median have stayed the exact same

We value consumer businesses on a multiple of Last Twelve Months (LTM) and Next Twelve Months (NTM) revenue. Multiples shown are calculated by taking the Enterprise Value / NTM revenue. In addition, we separated multiples by time period and by growth rate. High growth businesses are growing 40% NTM revenue; Mid-growth businesses are growing 20% NTM revenue, and Low-growth are less than 20% growth rate.

Breakdown of Historic Multiples

Multiples by Category

We have separated the multiples and outputs by subsector. On the upper end, consumer social commands the highest EV/NTM multiples, while e-commerce commands the lowest multiples.

Multiples by Growth Category

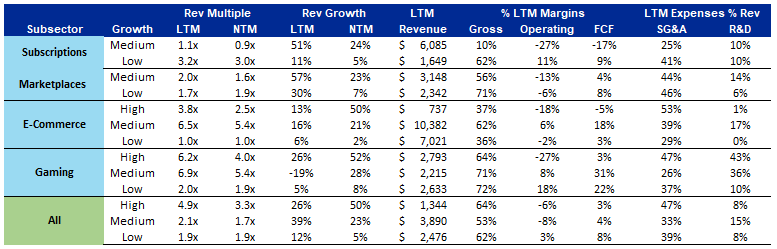

Subsector Output

Please send any feedback or suggestions to insights@cobalt.la.

Written by Ben Futoriansky.

Certain information contained in here has been obtained from third-party sources and Cobalt has not independently verified such information and we make no representations about the accuracy of the information contained in this blog, links to third party sources or the materials provided by such sources. The content in this blog is for informational purposes only and should not be relied upon as investment advice or recommendations of any kind. In addition, nothing contained in this blog should be relied upon for purposes of investing in any funds managed by Cobalt Capital, nor is anything contained herein an offering to invest in any Cobalt Capital fund — any such offering will be set forth in a legal agreement provided directly by Cobalt Capital.

The content in this blog speaks only as of the date indicated. Any projections, estimates, forecasts, targets, prospects, and/or opinions expressed in these materials are subject to change without notice and may differ or be contrary to opinions expressed by others.